·

Rising gold prices led to a significant expansion in gold loans,

contributing to healthy retail credit growth in the post-festive period

·

The share of younger borrowers within the

first-time borrower segment increased, particularly in consumer durable loans

and personal loans

·

Retail credit growth, boosted by the rationalisation

of Goods and Services Tax (GST) rates, stabilised, notably from the second

month after the festive period

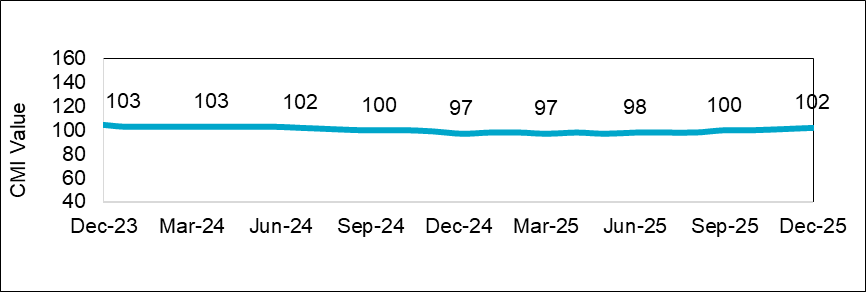

Mumbai – India’s Credit Market Indicator (CMI)1 rose in the December

2025 quarter both year-over-year (YoY) and quarter-over-quarter (QoQ),

supported by strong growth in gold loans amid a sharp increase in global gold

prices. However, retail credit supply normalised in the post-festive period, easing

from the momentum created by the rationalisation of Goods and Services Tax

(GST) and returning to end of 2024 levels, indicating a seasonal moderation in

short-term demand.

TransUnion CIBIL’s March 2026 Credit

Market Report indicates that the Consumer Credit Market Indicator

(CMI) increased to 102 for the quarter ended December 2025, up from 97 in the

quarter ended December 2024.The December 2025 CMI is also higher by two points

from 100 in the preceding quarter of September 2025. The December 2025 quarter CMI

marked the third consecutive quarter of improvement.

The CMI is a

comprehensive measure of data elements that are summarised monthly to analyse

changes in credit market health, categorised under four pillars: demand,

supply, consumer behaviour, and performance. These factors are combined into a

single, comprehensive CMI indicator, and can also be viewed in more detail

individually. A higher CMI reading indicates improving credit market health, whereas

a lower reading indicates a decline.

“There is

evidence of a shift in retail credit growth dynamics, with momentum extending

beyond secured products such as gold loans to rising consumption demand from

first-time and younger borrowers. While the post-festive moderation in credit

supply reflects seasonal trends, the overall improvement in credit performance

reinforces the strength and maturity of India’s credit market,’’ said Mr.

Bhavesh Jain, MD and CEO, TransUnion CIBIL.

Chart

1: Credit Market Indicator (CMI) Dec 2023 – Dec 2025

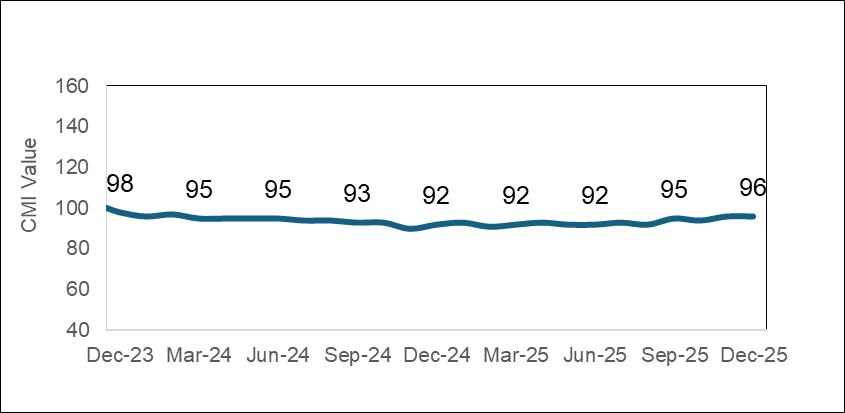

Non-metro

Geographies, New-to-Credit2 Consumers Drive Credit Demand

The CMI for

demand increased to 96 in the December 2025 quarter from 92 in the December

2024 quarter, buoyed by strong demand from semi-urban and rural consumers.

Their share of the total retail borrower base rose to 54%, an increase of three

percentage points over the year-ago period. The share of New-to-Credit

consumers also increased by one percentage point to 15% of total borrowers.

During the

post-festive period, auto loan volumes improved in line with last year’s

levels, primarily supported by increased supply in the affordable mid‑segment car category (INR 5–10 lakh). In the post festive

period, the average daily supply grew by 10% in auto loans in 2025, compared to

2024.

Chart

2: CMI for Demand Dec 2023 – Dec 2025

“The continued

expansion of credit demand in non-metro and semi-urban markets underscores the

structural shift underway in India’s lending landscape. As access to formal

credit deepens beyond traditional urban centres, we are seeing a more

geographically diversified borrower base emerge. This trend reflects improving

credit awareness enhanced distribution by lenders and the growing relevance of

tailored products for these segments, all of which are contributing to a more

inclusive and balanced credit ecosystem,’’ Mr. Jain said.

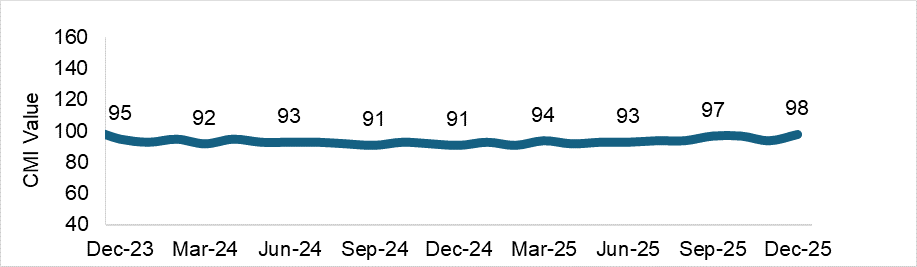

Credit

Supply Increases on the Back of Gold Loans

The CMI for

supply rose to 98 in the December 2025 quarter from 91 in the December 2024

quarter, largely driven by a significant increase in both the volume and value

of gold loans. This growth was supported by higher-ticket gold loans availed by

consumers seeking to benefit from rising gold prices.

Since March 2023,

the average gold loan ticket size has increased by 1.8X times driving a sharp

rise in origination value. The indexed growth (indexed to March 2023) in the

gold loan average ticket size touched 189 points in the quarter ended December

2025, compared to 132 in the quarter-ended December 2024. The average ticket

size for the three months ended December 2025 stands at INR 1.9 lakh. Gold loans

now represent the largest share by volume (36%) and value (39%) among all

retail loan categories, accounting for more than one third of the total retail

loan supply. In terms of outstanding balances, gold loans are now second only to

housing loans.

From a geographic

and demographic perspective, gold loans are expanding beyond their traditional concentration

in southern states and seeing higher growth in northern and western states. For

instance, as of December 2025, the three states with above average YoY growth

rates in gold loan origination volumes were Uttar Pradesh – 96%, Madhya Pradesh

– 80% and Rajasthan – 79%. Additionally, more than half, 54%, are being utilised

by prime and above consumers indicating a more diverse credit profile. This trend

also highlights the growing acceptance of gold loans as a mainstream retail

credit product.

Chart

3: CMI for Supply Dec 2023 – Dec 2025

Consumption-led

Credit Revives First-Time Borrower Segment

The

first-time-borrowers (FTB)3 segment grew 7% by originating consumers

YoY in the December 2025 quarter, supported by strong momentum in consumption-led

credit. Within this segment, personal loans recorded a 20% YoY increase,

compared to a 3% decline in the quarter ended December 2024. Similarly, consumer

durable loans grew 22% YoY, reversing an 11% decline in the year-ago period.

Additionally,

borrowers below 35 years old increased by 17% YoY in the December 2025 quarter,

compared to a 3% decrease in the December 2024 quarter. This group now constitutes

58% of the FTB segment, and is a key contributor towards its overall growth.

CMI

for Performance Increases by Six Points

Improved balance

level 90+ days past due (DPD) delinquencies across key product segments led to

the CMI for performance increasing by six points to 107 in December 2025, from 101

in December 2024. The micro-loan against property (LAP) segment was the only

category to exhibit some stress, with balance-level 90+ DPD delinquency increasing

by 35 basis points YoY to 3.1% in December 2025. Despite this increase,

delinquency levels have remained broadly stable and range‑bound since the previous quarter.

“India’s retail

credit landscape continues to demonstrate resilience and structural depth,

supported by a healthy balance between consumption-led demand and improving

credit performance. Higher

origination volumes in home, auto, and consumer durable loans point to a steady

shift toward asset-backed borrowing. Concurrently, rising average loan sizes

and a growing share of prime and above borrowers indicate sustained lender

focus towards credit tested profiles. This reflects evolving borrower

preferences as well as lenders’ ability to adapt to changing credit requirements.

“At the same

time, rising participation from first-time borrowers, younger consumers, and

non-metro geographies points to a broader formalisation of credit and

increasing financial inclusion. As the ecosystem matures, maintaining a strong focus

on credit discipline and risk management will remain critical to ensure sustainable

long-term growth,’’ said Mr. Jain.